All Categories

Featured

Table of Contents

So it is not mosting likely to be some magic path to wide range. It will assist you make a little extra on your cash long-term. Naturally, there are other advantages to any type of entire life insurance coverage plan. There is the death benefit. While you are attempting to reduce the ratio of premium to fatality advantage, you can not have a plan with zero death advantage.

Some individuals selling these plans argue that you are not disrupting compound passion if you obtain from your plan rather than withdraw from your financial institution account. The money you obtain out makes nothing (at bestif you do not have a clean funding, it might also be costing you).

That's it. Not so hot currently is it? A great deal of individuals that acquire right into this principle additionally purchase into conspiracy theory concepts about the world, its federal governments, and its banking system. IB/BOY/LEAP is positioned as a method to in some way avoid the world's monetary system as if the globe's largest insurer were not component of its financial system.

It is spent in the general fund of the insurance policy firm, which mostly spends in bonds such as US treasury bonds. You obtain a bit higher passion price on your cash (after the very first couple of years) and possibly some possession security. Like your financial investments, your life insurance policy need to be boring.

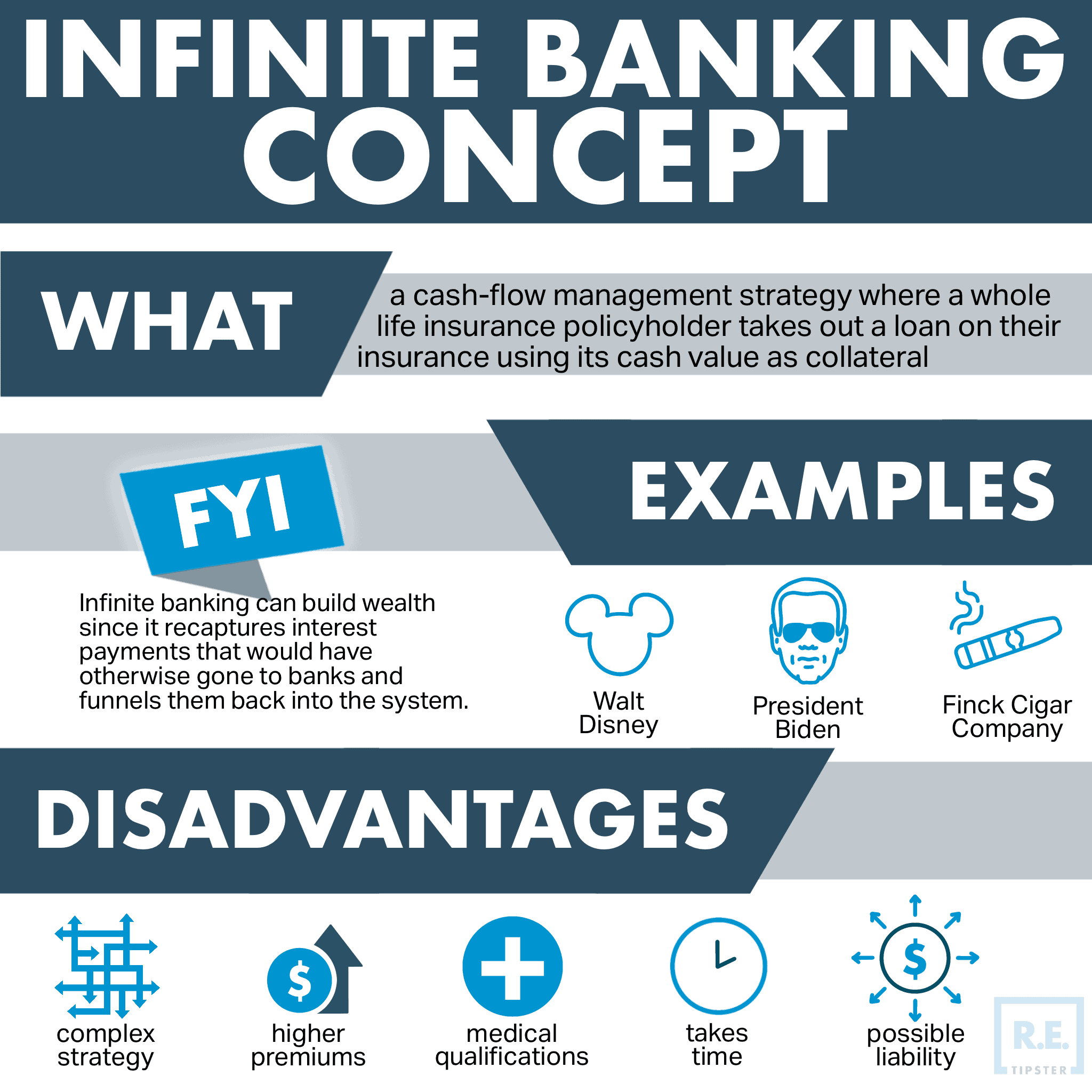

Infinite Banking System

It feels like the name of this idea modifications as soon as a month. You may have heard it referred to as a perpetual riches technique, household financial, or circle of riches. Regardless of what name it's called, infinite financial is pitched as a secret way to construct riches that just abundant individuals learn about.

You, the insurance policy holder, placed cash into a whole life insurance plan via paying premiums and purchasing paid-up enhancements.

Cash Value Life Insurance Infinite Banking

The whole idea of "financial on yourself" only works due to the fact that you can "bank" on yourself by taking car loans from the plan (the arrow in the chart over going from whole life insurance policy back to the insurance policy holder). There are two various sorts of lendings the insurance provider may supply, either direct recognition or non-direct recognition.

One feature called "wash loans" sets the rates of interest on fundings to the same price as the returns rate. This implies you can obtain from the policy without paying passion or getting rate of interest on the quantity you obtain. The draw of boundless financial is a returns rate of interest and guaranteed minimum price of return.

The drawbacks of infinite banking are commonly neglected or not stated in all (much of the details readily available concerning this idea is from insurance coverage representatives, which might be a little prejudiced). Just the cash money value is growing at the dividend price. You likewise have to pay for the cost of insurance, fees, and expenses.

Every irreversible life insurance plan is different, but it's clear a person's total return on every buck invested on an insurance coverage product could not be anywhere close to the reward rate for the policy.

Whole Life Insurance Infinite Banking

To give a very standard and hypothetical instance, let's presume someone has the ability to gain 3%, usually, for each dollar they invest on an "infinite financial" insurance coverage item (after all costs and fees). This is double the approximated return of whole life insurance policy from Customer News of 1.5%. If we presume those dollars would certainly go through 50% in taxes total if not in the insurance policy product, the tax-adjusted price of return can be 4.5%.

We think greater than average returns overall life product and a really high tax obligation rate on dollars not put into the policy (which makes the insurance policy item look much better). The fact for lots of folks may be worse. This fades in contrast to the long-term return of the S&P 500 of over 10%.

Infinite Banking Concept Example

At the end of the day you are acquiring an insurance policy product. We like the defense that insurance policy offers, which can be gotten a lot less expensively from an affordable term life insurance coverage plan. Overdue financings from the plan may additionally minimize your death benefit, decreasing another degree of security in the plan.

The concept only works when you not just pay the substantial costs, yet use additional money to purchase paid-up additions. The possibility cost of all of those dollars is significant exceptionally so when you could rather be purchasing a Roth Individual Retirement Account, HSA, or 401(k). Also when compared to a taxable investment account and even an interest-bearing account, infinite financial might not provide equivalent returns (compared to spending) and similar liquidity, accessibility, and low/no cost framework (contrasted to a high-yield savings account).

When it concerns economic preparation, entire life insurance policy usually attracts attention as a preferred choice. There's been a growing fad of advertising and marketing it as a device for "limitless banking." If you've been exploring entire life insurance policy or have actually encountered this principle, you might have been informed that it can be a means to "become your very own financial institution." While the concept could seem appealing, it's crucial to dig deeper to understand what this actually implies and why checking out whole life insurance policy by doing this can be deceptive.

The concept of "being your very own financial institution" is appealing since it recommends a high level of control over your financial resources. This control can be imaginary. Insurer have the ultimate say in exactly how your policy is handled, consisting of the regards to the fundings and the rates of return on your cash worth.

If you're considering entire life insurance policy, it's vital to see it in a wider context. Whole life insurance policy can be a valuable device for estate planning, giving an ensured survivor benefit to your beneficiaries and potentially supplying tax benefits. It can also be a forced cost savings automobile for those that battle to save money continually.

Nelson Nash Bank On Yourself

It's a kind of insurance coverage with a financial savings part. While it can supply stable, low-risk growth of money value, the returns are generally lower than what you might accomplish through other investment lorries. Prior to delving into whole life insurance coverage with the idea of limitless financial in mind, take the time to consider your economic objectives, threat tolerance, and the full variety of monetary products available to you.

Infinite banking is not a monetary remedy. While it can function in particular situations, it's not without risks, and it requires a substantial commitment and comprehending to take care of efficiently. By recognizing the prospective mistakes and understanding the real nature of whole life insurance, you'll be better equipped to make an enlightened choice that supports your financial wellness.

This book will certainly teach you just how to establish a banking policy and exactly how to make use of the financial plan to buy realty.

Boundless financial is not an item or solution used by a particular institution. Boundless financial is a technique in which you purchase a life insurance coverage policy that gathers interest-earning money value and get car loans against it, "obtaining from yourself" as a resource of capital. After that ultimately repay the finance and start the cycle all over once again.

Pay policy premiums, a part of which constructs cash money worth. Take a finance out against the plan's money worth, tax-free. If you utilize this principle as intended, you're taking cash out of your life insurance plan to acquire whatever you would certainly require for the remainder of your life.

{kind=link}

Latest Posts

Nash Infinite Banking

Infinite Banking With Whole Life Insurance

Privatized Banking Concept